Submitted by admin on June 7th, 2026

When used properly, taking out a loan can be a useful financial instrument. Loans can assist you in meeting important goals such as paying for a medical emergency, home improvement, education, or debt consolidation, among other things. But if borrowing without planning can cause financial problems. It is crucial to know how to borrow responsibly to stay ahead of your debt and maintain good financial health.

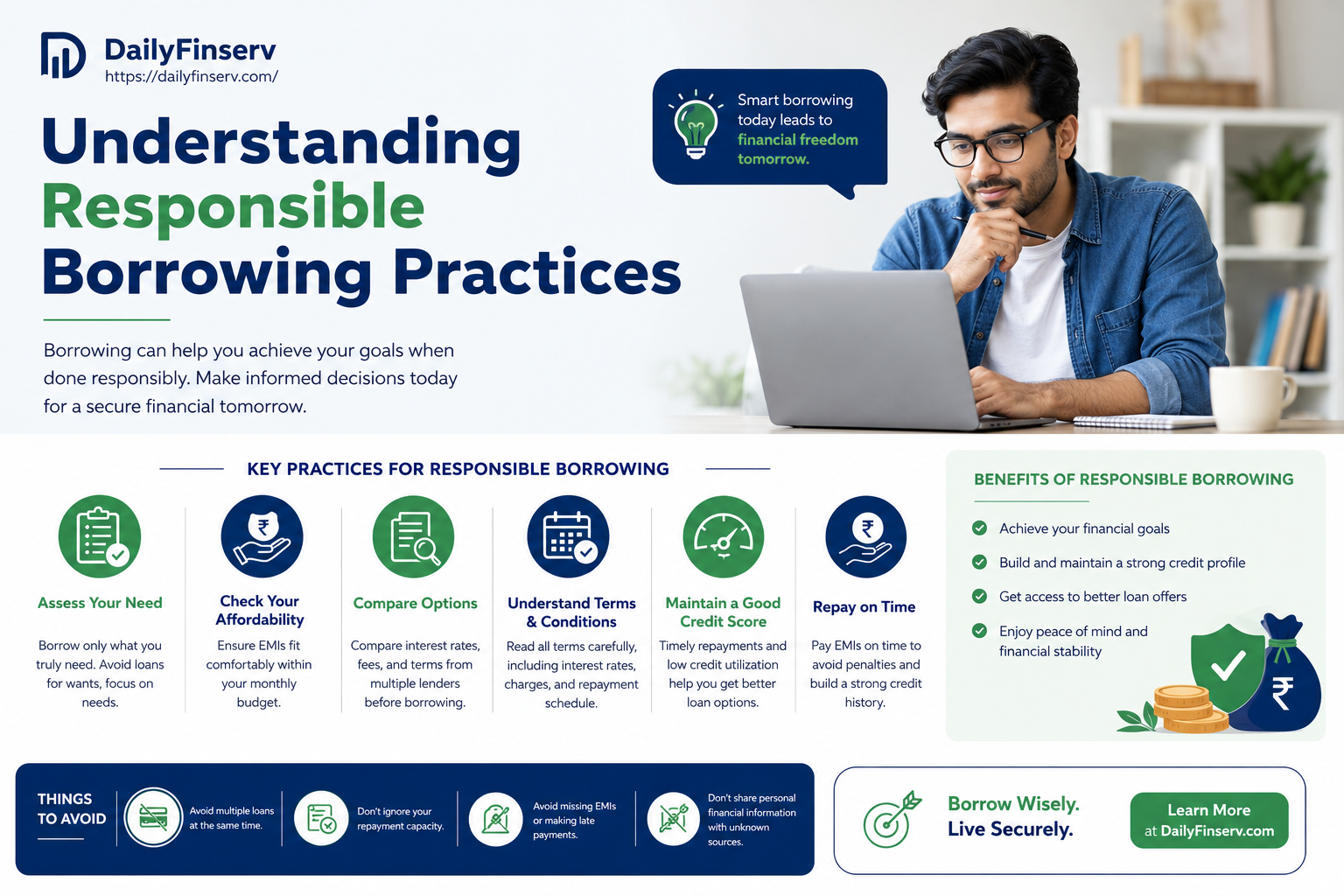

Avoid borrowing more than the need be is one of the most important borrowing principles. Lenders will be willing to approve you for a higher loan, but that’s not an indication that you should take out the maximum possible.

Go through the process of assessing your real financial need and draw up a budget before you apply.

Evaluate your ability to get back the money.Evaluate your capacity to pay back the money.

If you are considering taking on a loan, check out your monthly income and expenses first. Consider your ability to afford the EMI, and your other financial commitments.

Not all loans are the same. The interest rate, repayment periods, fees and conditions of the loan vary between lenders.

When you are ready to make a choice, shop around:

Shop around and research to locate a loan that suits your needs and financial situation.

Many borrowers only pay attention to the monthly payment and the specifics of the loan agreement are ignored. When taking out a loan, it is essential to know all the terms and conditions of the loan before you sign.

Carefully read through the loan terms and ask questions if there are any that are unclear. Understanding the loan details can avoid any potential unpleasantness down the road and additional expenses.

Your credit score is a key part to getting a loan approved and the rate that you will receive. Improved credit score can mean improved borrowability.

Making good on credit lessons are not just useful for responsible borrowing, however they can likewise enhance future financial chances.

Personal loans can have many uses but should not be taken out for frivolous purchases or unnecessary living costs. Taking on debt for unnecessary purchases can lead to no long-term benefit.

Make sure the purchase is necessary, and consider saving for it instead.

An established repayment plan helps make sure you make timely payments during the loan period. Establishing automatic payments, building up an emergency savings account, and keeping a close eye on your finances can minimize the chances of late payments.

Paying regularly will help to keep your credit score high and you’ll pay off your debt earlier.

Responsible borrowing is making sensible financial decisions and taking sensible debt management. With the tips to use loans effectively, without jeopardizing your financial future, you can use a loan without hurting your credit and be able to borrow only what you need. A smart way of borrowing helps to make credit work for you, not against you.

Int Rates : 10.5% - 22%

Loan Amount: ₹ 1,00,000.00

Maximum Tenure - 7 Years

Lowest EMI : ₹ 1,686

Interest Rate 13.99% - 24.99%

Loan Amount: ₹ 1,00,000.00

Maximum Tenure – 5 Years

Lowest EMI : ₹ 2,326

Interest Rate 9% - 13%

Loan Amount: ₹ 1,00,000.00

Maximum Tenure – 20 Years

Lowest EMI : ₹ 1,014

Interest Rate 8.40% - 12%

Loan Amount : ₹ 1,00,000.00

Maximum Tenure – 35 Years

Lowest EMI – ₹ 739