Submitted by admin on May 23rd, 2026

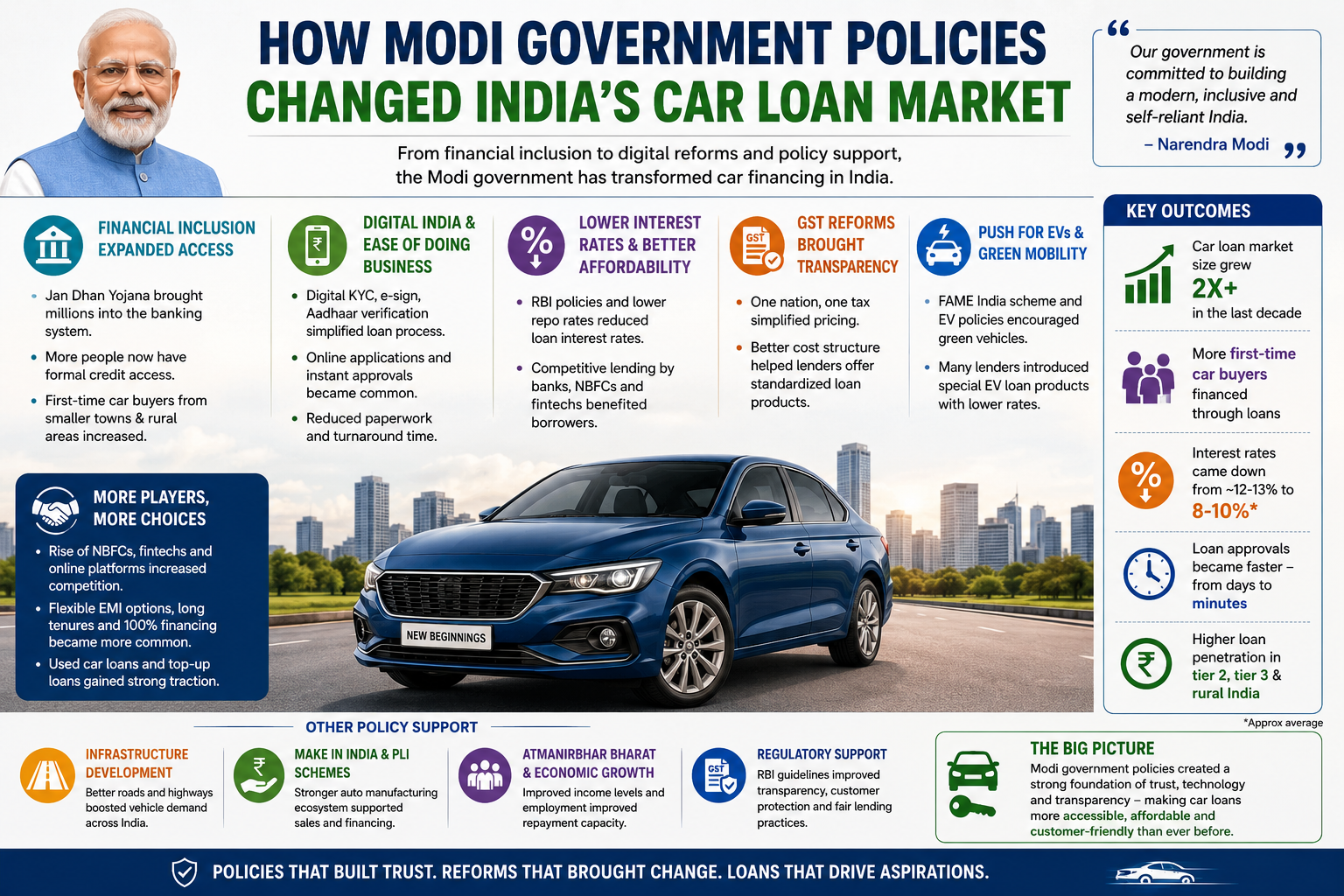

In the last ten years, the car loan market has seen significant changes in India, all thanks to various economic and financial policies that have been implemented during the regime of the Modi Government. These initiatives transformed Indian vehicle purchases and financing, ranging from digital banking to GST reforms and financial inclusion initiatives. Nowadays, car loans are more accessible, quicker and technologically advanced than ever before.

One of the major transformations has been through the Digital India program. Digital processes for customer verification, submission of documents, and loan processing were quickly embraced by banks and financial institutions.

This digital transformation was making life easier for all listed groups of consumers in the cities and in semi-urban areas, including salaried people, the self-employed and people purchasing their first car.

The government initiatives like PMJDY enabled millions of Indians to join the formal banking system. As more individuals opened bank accounts and started to create financial records, lenders discovered new customer bases.

Middle-class families, small business owners and rural consumers, who were unable to access formal credit, were now able to finance cars. Better banking penetration also incentivized many first time buyers to buy cars by availing the EMI financing options.

This growth contributed greatly to the rise in the demand for both fresh and second hand car loans in India.

Automobile industry was directly affected by the introduction of Goods and Services Tax (GST) in 2017. GST eliminated various direct and indirect taxes and provided a uniform tax regime throughout the country.

The ease in comparing on-road prices and EMI calculations was also beneficial for consumers.

The Modi government era witnessed the growth of Non Banking Financial Companies (NBFCs) and fintech companies in India. These institutions came up with flexible car loans, quicker approvals, and personalized EMI options.

Fintech lenders adopted digital assessment of credit, and extended loans to customers who have limited credit scores. These days, numerous programs offer prequalified auto loans in minutes via mobile apps.

There was also a battle between the banks, NBFC’s and fintech companies, which further assisted the borrowers to access better rates of interest and attractive loan repayment options.

The government’s policies and initiatives promoting electric vehicles (EVs) and the FAME India Scheme spurred financial institutions to develop loan products tailored for EVs.Financial institutions have started EV loan products in response to government initiatives and regulations that incentivized the adoption of electric vehicles, such as the FAME India Scheme. Several banks began to provide reduced interest rates and extended loan terms for EVs.

The rise in awareness of EVs spurred lenders to become more interested in green mobility financing, giving rise to a new category of car loans.

The market grew, but so did some economic events, and they had an impact on car loans. The demonetisation of the currency had a temporary dampening impact on vehicle sales because of a shortage of cash. Inflation and an increase in the prices of fuels and interest rates later on made EMI heavy for many borrowers.

Modi government policies made a significant change in the Indian car loan market by encouraging digital banking, financial inclusion, the growth of fintech and transparent tax systems. Today, car financing in India is no longer a time-consuming and difficult process, but is now quicker, easier, and more technologically advanced.

Int Rates : 10.5% - 22%

Loan Amount: ₹ 1,00,000.00

Maximum Tenure - 7 Years

Lowest EMI : ₹ 1,686

Interest Rate 13.99% - 24.99%

Loan Amount: ₹ 1,00,000.00

Maximum Tenure – 5 Years

Lowest EMI : ₹ 2,326

Interest Rate 9% - 13%

Loan Amount: ₹ 1,00,000.00

Maximum Tenure – 20 Years

Lowest EMI : ₹ 1,014

Interest Rate 8.40% - 12%

Loan Amount : ₹ 1,00,000.00

Maximum Tenure – 35 Years

Lowest EMI – ₹ 739