Submitted by admin on May 22nd, 2026

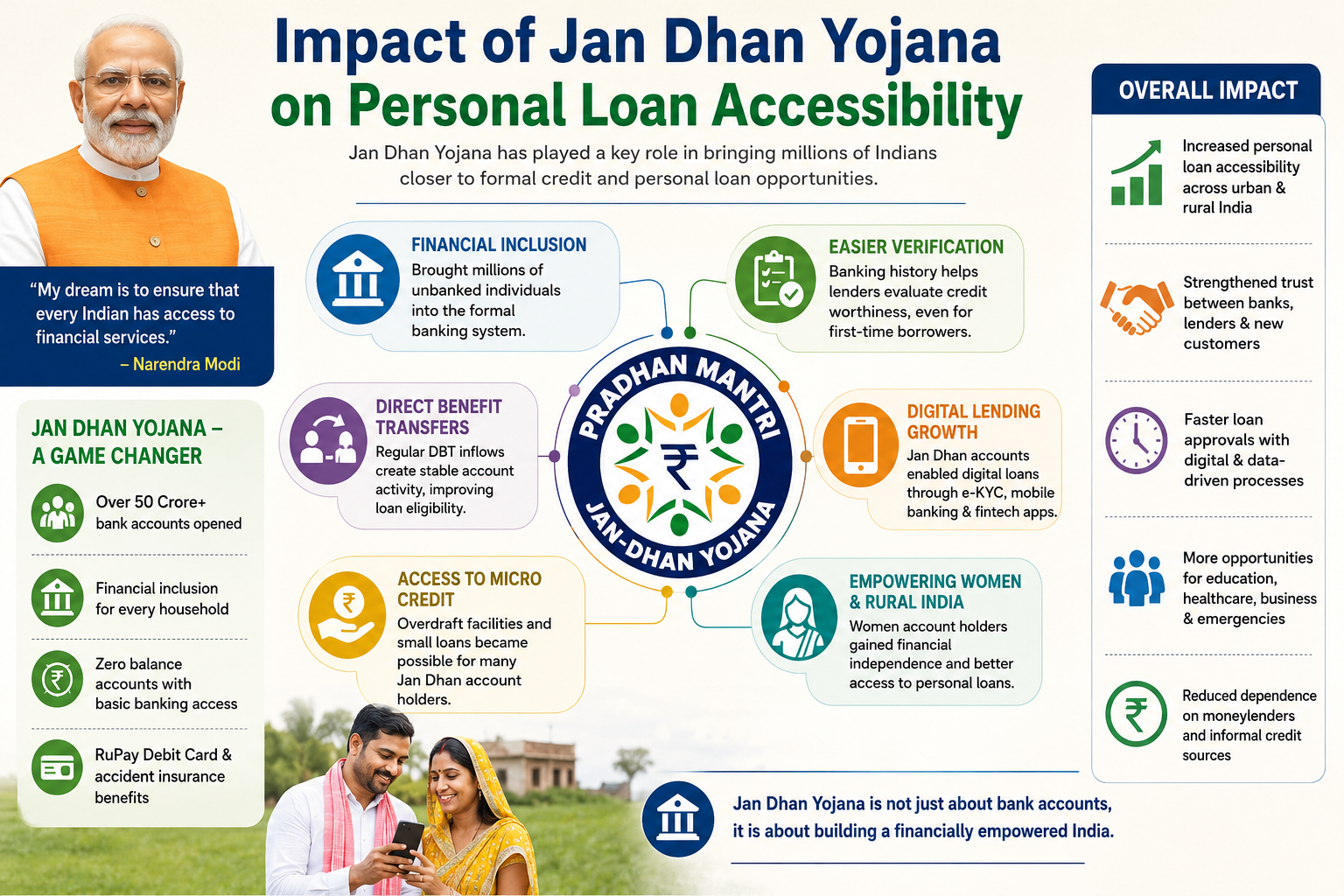

Introduction of banks in the country through Pradhan Mantri Jan Dhan Yojana (PMJDY) in 2014 revolutionized the banking and financial landscape of the country. The objective of the scheme was to formalise the banking system, so that all households could become a part of it. Jan Dhan Yojana had made a huge difference in the accessibility of personal loans, particularly for the low-income population, rural areas, and first-time borrowers over the years.

A primary obstacle when it comes to loan approval is to verify the financial history of the applicant. Jan Dhan accounts resolved this issue by developing transaction history and banking records for millions of people.

The use of account activity, direct benefit transfers, and savings patterns to determine loan eligibility is something that banks and fintech companies have been doing lately. Sometimes, even those who don’t have traditional salary slips or income proof can be eligible for small personal loans because of their banking behaviour.

This has particularly helped the daily wage earners, small traders, farmers and self-employed workers.

Many of the Government’s subsidy and welfare payments are made directly into bank accounts under Jan Dhan Yojana. The system provided better transparency and prevented leakage of funds.

When government money was regularly deposited in the accounts, there were stable transactions. The activity is beneficial to lenders when they review loan applications. You can be more likely to obtain a little bit loan or overdraft facility if you’re using the same account repeatedly.

This was the first time that many families could access formal credit.

Jan Dhan Yojana also helped in the development of digital banking in India. It, along with Aadhaar and Mobile connectivity, paved the way for the JAM trinity, Jan Dhan, Aadhaar, and Mobile.

This digital environment made application for an online loan easier and quicker. Nowadays, numerous banks and fintech companies are offering personal loans instantly by utilizing e-KYC and digital verification techniques connected to Jan Dhan accounts.

Now, with the new loan facility, rural and semi-urban borrowers can obtain loans without having to visit bank branches several times. This has minimized the paperwork and made it easier to make financial transactions.

The Jan Dhan account holders were able to avail overdraft and micro credit. Loans for health care, education, home repairs and living expenses were more readily available.

Financial independence was enhanced, especially for the benefit of women account holders. Banking services also helped people save money and manage their finances.

There are still some issues to be addressed as a result of this positive impact. There is a significant number of Jan Dhan accounts which remain unutilized and in some areas the financial literacy is still low. Unstable incomes are another problem faced by some borrowers that makes it difficult to pay back the loan.

Further, uneducated financial sensibilities can also result in over-borrowing with easy digital loans. Responsible lending and appropriate financial education are still crucial for sustainable development.

Jan Dhan Yojana has contributed significantly in the field of making personal loan accessible in India. The scheme widened the scope of financial services, generated financial identities and enabled digital lending, connecting millions of people to formal financial systems. In conclusion, Jan Dhan accounts will continue to play a crucial role in a digitally evolving India, ensuring that personal lending is inclusive and accessible for all.

Int Rates : 10.5% - 22%

Loan Amount: ₹ 1,00,000.00

Maximum Tenure - 7 Years

Lowest EMI : ₹ 1,686

Interest Rate 13.99% - 24.99%

Loan Amount: ₹ 1,00,000.00

Maximum Tenure – 5 Years

Lowest EMI : ₹ 2,326

Interest Rate 9% - 13%

Loan Amount: ₹ 1,00,000.00

Maximum Tenure – 20 Years

Lowest EMI : ₹ 1,014

Interest Rate 8.40% - 12%

Loan Amount : ₹ 1,00,000.00

Maximum Tenure – 35 Years

Lowest EMI – ₹ 739