Submitted by admin on April 12th, 2026

Financial crises may crop up unannounced in the times of war or economic crisis. Healthcare demands, loss of employment or emergency repairs might compel people to borrow money immediately. Personal loans in case of emergency can be used to obtain some quick relief, although personal loans to borrow in times of uncertainty should be taken seriously. The financial future of your business is safeguarded by knowing when to borrow money, and when it is better not to take a loan.

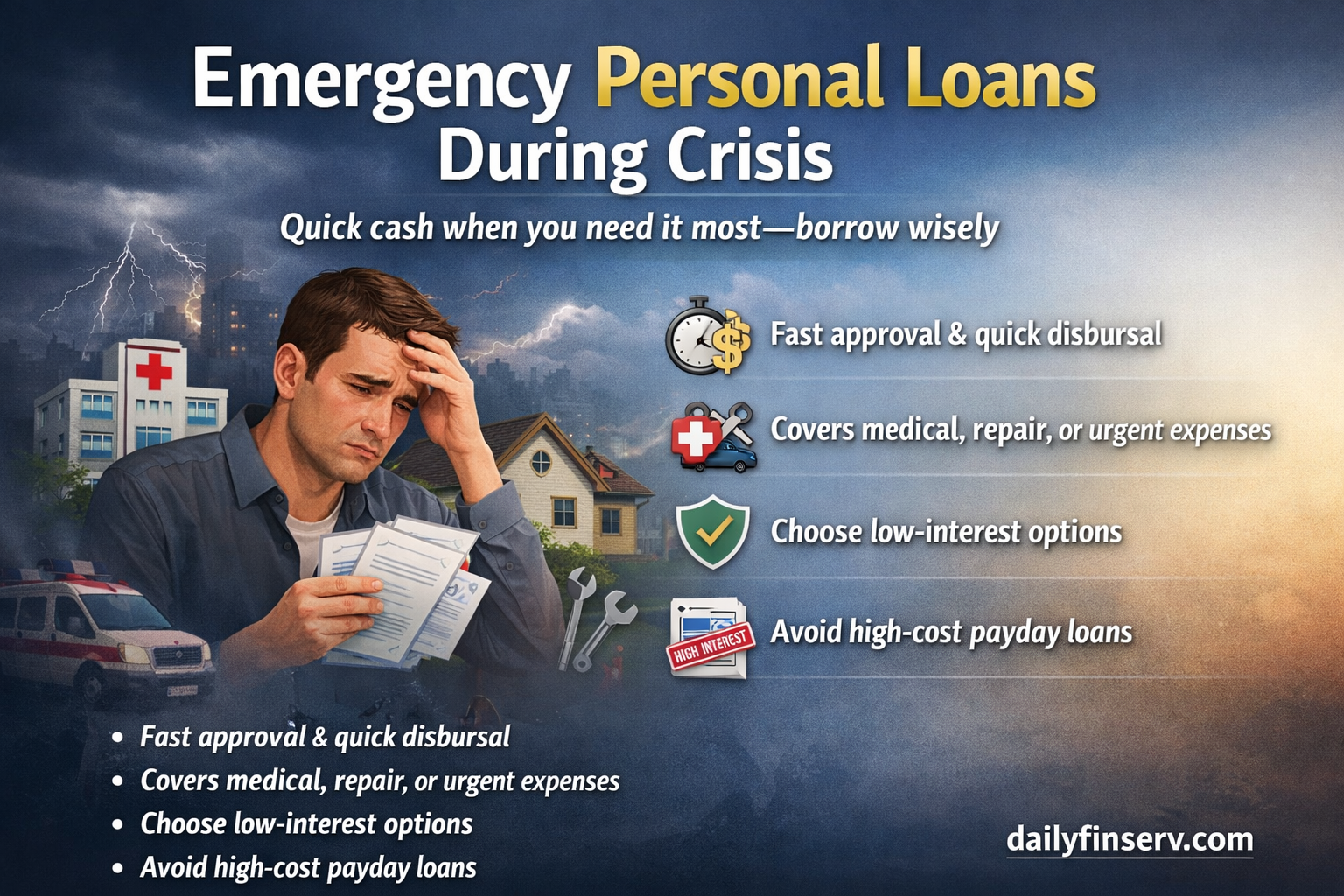

Emergency loans can be applied in cases where the cost is necessary and inevitable. Borrowing is justified in cases such as medical emergencies or emergency need to repair the house or even in case of temporary gaps in income. A personal loan will assist you to attend to the emergency needs without interfering with your life in such instances.

Another valid reason to borrow is debt consolidation. In case you have more than one high-interest debts, by rolling them all into a personal loan with a lower interest rate, the monthly payments will be reduced and you will find it easier to pay off.

It is also rational to borrow when your income is constant or you have a definite repayment schedule. A loan can be a short-term option in case you are sure you can meet EMIs without compromising on the key expenditures.

When faced with a crisis, one should not borrow money to spend on unnecessary luxuries like having a luxurious life, going on holidays or upgrading his lifestyle. These may add to financial pressure without value addition.

You must not borrow money too, when you have an uncertain income. Repayment may be challenging in these situations and as a result, penalties, damage to a credit score and long term debt issues may occur.

Loans with high interest rates or those that present some hidden fee ought to be treated with care. When the interest rate on borrowing is excessively high, it will aggravate your financial condition rather than improve it.

Also, borrowing more than one loan at a time may lead to a debt trap. When dealing with a number of EMIs, it may not take long to become overwhelming, when faced with an economic downturn.

Assess your financial status before applying to an emergency personal loan. Examine your monthly earnings, current liabilities and necessary expenditures. Make sure that the EMI is within your pocket.

Compare various lenders to get good interest rates and easy repayment terms. Ensuring that you read the terms and conditions carefully will make you not run into unnecessary bills.

It is also prudent to consider other options like using savings, finding a family source or negotiating payment terms prior to borrowing money.

In case you choose to borrow money, borrow only what you need. Select a term of repayment that is affordable and has a total interest amount. Keep a high credit rating in order to obtain more favorable loan conditions.

Automatic payments can help you to save missed EMIs and penalties. In case you change your financial position, you should inform your lender as soon as possible so that you could discuss the possibility of restructuring.

Emergency personal loans may be a good financial instrument in case of a crisis, but only in case of responsible usage. The trick is to borrow with a good intention, with a good plan of repayment and with restraint.

Looking towards an emergency personal loan and want a secure solution then consider your options with Daily Finserv. To visit dailyfinserv.com and get flexible and customized loans that will help you during the uncertain times.

Int Rates : 10.5% - 22%

Loan Amount: ₹ 1,00,000.00

Maximum Tenure - 7 Years

Lowest EMI : ₹ 1,686

Interest Rate 13.99% - 24.99%

Loan Amount: ₹ 1,00,000.00

Maximum Tenure – 5 Years

Lowest EMI : ₹ 2,326

Interest Rate 9% - 13%

Loan Amount: ₹ 1,00,000.00

Maximum Tenure – 20 Years

Lowest EMI : ₹ 1,014

Interest Rate 8.40% - 12%

Loan Amount : ₹ 1,00,000.00

Maximum Tenure – 35 Years

Lowest EMI – ₹ 739